8 State-space models

Jan-Ole Fischer

State_space_models.RmdBefore diving into this vignette, we recommend reading the vignettes Introduction to LaMa and Automatic differentiation via RTMB.

This vignette shows how to fit state-space models which can be interpreted as generalisation of HMMs to continuous state spaces. Several approaches exist to fitting such models, but Langrock (2011) showed that very general state-space models can be fitted via approximate maximum likelihood estimation, when the continuous state space is finely discretised. This is equivalent to numerical integration over the state process using midpoint quadrature.

Here, we will showcase this approach for a basic stochastic volatility model which, while being very simple, captures most of the stylised facts of financial time series. In this model the unobserved marked volatility is described by an AR(1) process:

g_t = \phi g_{t-1} + \sigma \eta_t, \qquad \eta_t \sim N(0,1), with autoregression parameter \phi < 1 and dispersion parameter \sigma. Share returns y_t can then be modelled as y_t = \beta \epsilon_t \exp(g_t / 2), where \epsilon_t \sim N(0,1) and \beta > 0 is the baseline standard deviation of the returns (when g_t is in equilibrium), which implies y_t \mid g_t \sim N(0, (\beta e^{g_t / 2})^2).

Example: stochastic volatility model

Simulating data

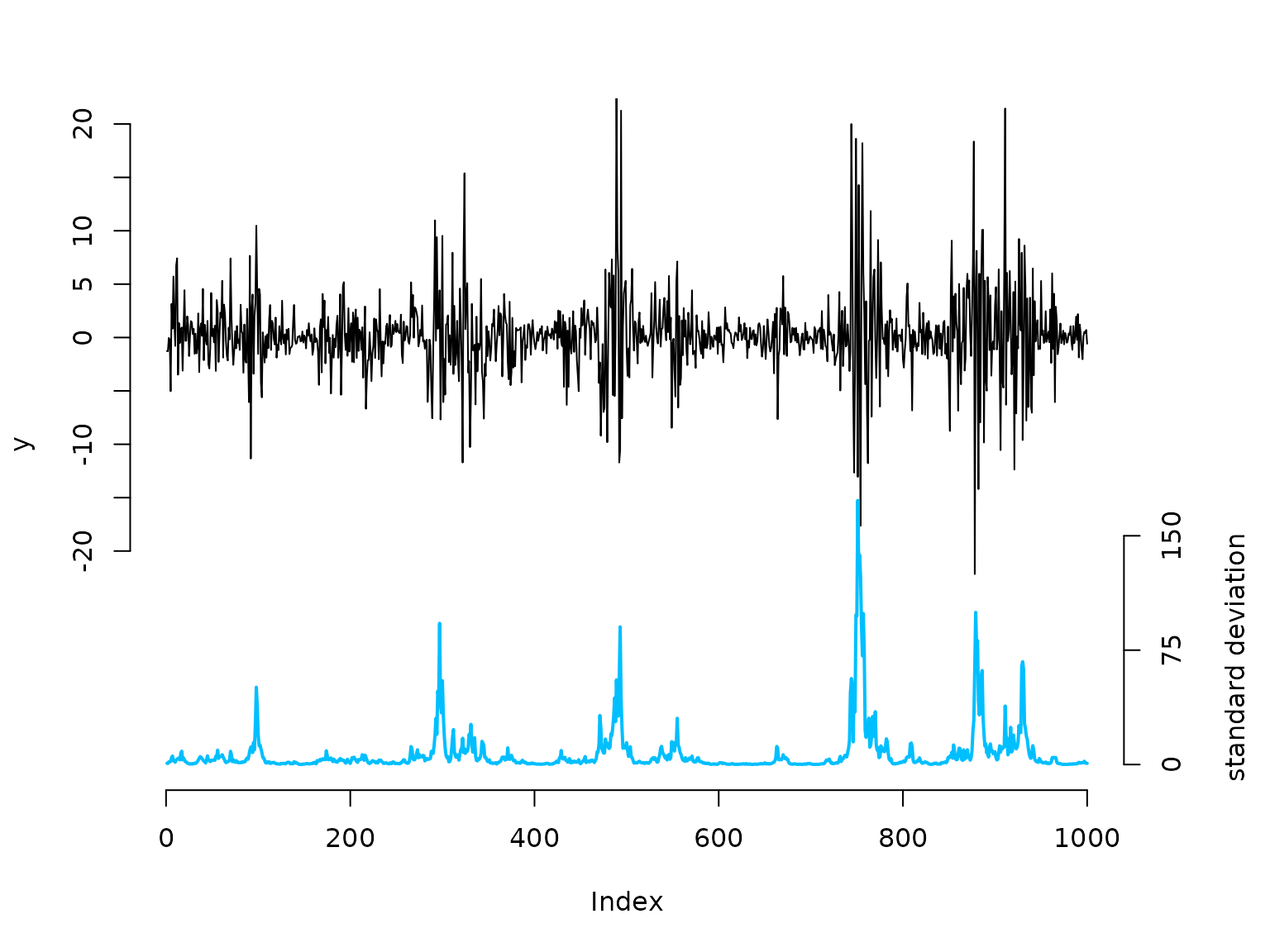

We start by simulating data from the above specified model:

beta = 2 # baseline standard deviation

phi = 0.95 # AR parameter of the log-volatility process

sigma = 0.5 # variability of the log-volatility process

n = 1000

set.seed(123)

g = rep(NA, n)

g[1] = rnorm(1, 0, sigma / sqrt(1-phi^2)) # stationary distribution of AR(1) process

for(t in 2:n){

# sampling next state based on previous state and AR(1) equation

g[t] = rnorm(1, phi*g[t-1], sigma)

}

# sampling zero-mean observations with standard deviation given by latent process

y = rnorm(n, 0, beta * exp(g/2))

# share returns

color = LaMaColors(2)

oldpar = par(mar = c(5,4,3,4.5)+0.1)

plot(y, type = "l", bty = "n", ylim = c(-40,20), yaxt = "n")

# true underlying standard deviation

lines(beta*exp(g)/7 - 40, col = color[2], lwd = 2)

axis(side=2, at = seq(-20,20,by=5), labels = seq(-20,20,by=5))

axis(side=4, at = seq(0,150,by=75)/7-40, labels = seq(0,150,by=75))

mtext("standard deviation", side=4, line=3, at = -30)

par(oldpar)Writing the negative log-likelihood function

To calculate the likelihood, we need to integrate over the state

space. We approximate this high-dimensional integral using a midpoint

quadrature which ultimately results in a fine discretisation of the

continuous state space into the intervals b with width

h and midpoints bstar (Langrock

2011). Thus, the likelihood below corresponds to a basic HMM

likelihood with a large number of states.

nll = function(par) {

getAll(par, dat)

phi = plogis(logit_phi); REPORT(phi)

sigma = exp(log_sigma); REPORT(sigma)

beta = exp(log_beta); REPORT(beta)

b = seq(-bm, bm, length = m + 1) # intervals for midpoint quadrature

h = b[2] - b[1] # interval width

bstar = (b[-1] + b[-(m+1)]) / 2 # interval midpoints

# approximating t.p.m. via midpoint quadrature

Gamma = sapply(bstar, dnorm, mean = phi * bstar, sd = sigma) * h

# stationary distribution of the AR(1) process: g ~ N(0, sigma^2/(1-phi^2))

delta = h * dnorm(bstar, 0, sigma / sqrt(1 - phi^2))

# state-dependent densities: y_t | g_t ~ N(0, (beta * exp(g_t/2))^2)

allprobs = t(sapply(y, dnorm, mean = 0, sd = beta * exp(bstar / 2)))

-forward(delta, Gamma, allprobs)

}Fitting an SSM to the data

Because the transition matrix \Gamma

is 100 \times 100 and dense, we set

TapeConfig(matmul = "atomic") before building the AD

objective.

By default ("plain"), RTMB unwraps every

matrix multiplication into all its individual scalar operations on the

tape. This is efficient when matrices are sparse, since the tape can

exploit the structure. For large, dense matrices it produces an enormous

tape — one scalar entry per element of the result — which slows both

tape construction and subsequent gradient evaluation.

Declaring matrix multiplications as atomic treats

each one as a single operation on the tape, keeping it compact

regardless of matrix size. If your transition matrix were sparse — for

example in models with local state dependence — the default

"plain" setting would be preferable.

TapeConfig(matmul = "atomic")

bm = 5 # truncation of state space at ±bm

m = 100 # number of quadrature points

par = list(

logit_phi = qlogis(0.95),

log_sigma = log(0.3),

log_beta = log(1)

)

dat = list(y = y, bm = bm, m = m)

obj = MakeADFun(nll, par, silent = TRUE)

system.time(

opt <- nlminb(obj$par, obj$fn, obj$gr)

)

#> user system elapsed

#> 0.659 0.000 0.660

mod = report(obj)Results

mod$phi # true: 0.95

#> [1] 0.951655

mod$sigma # true: 0.5

#> [1] 0.4436881

mod$beta # true: 2

#> [1] 2.18407

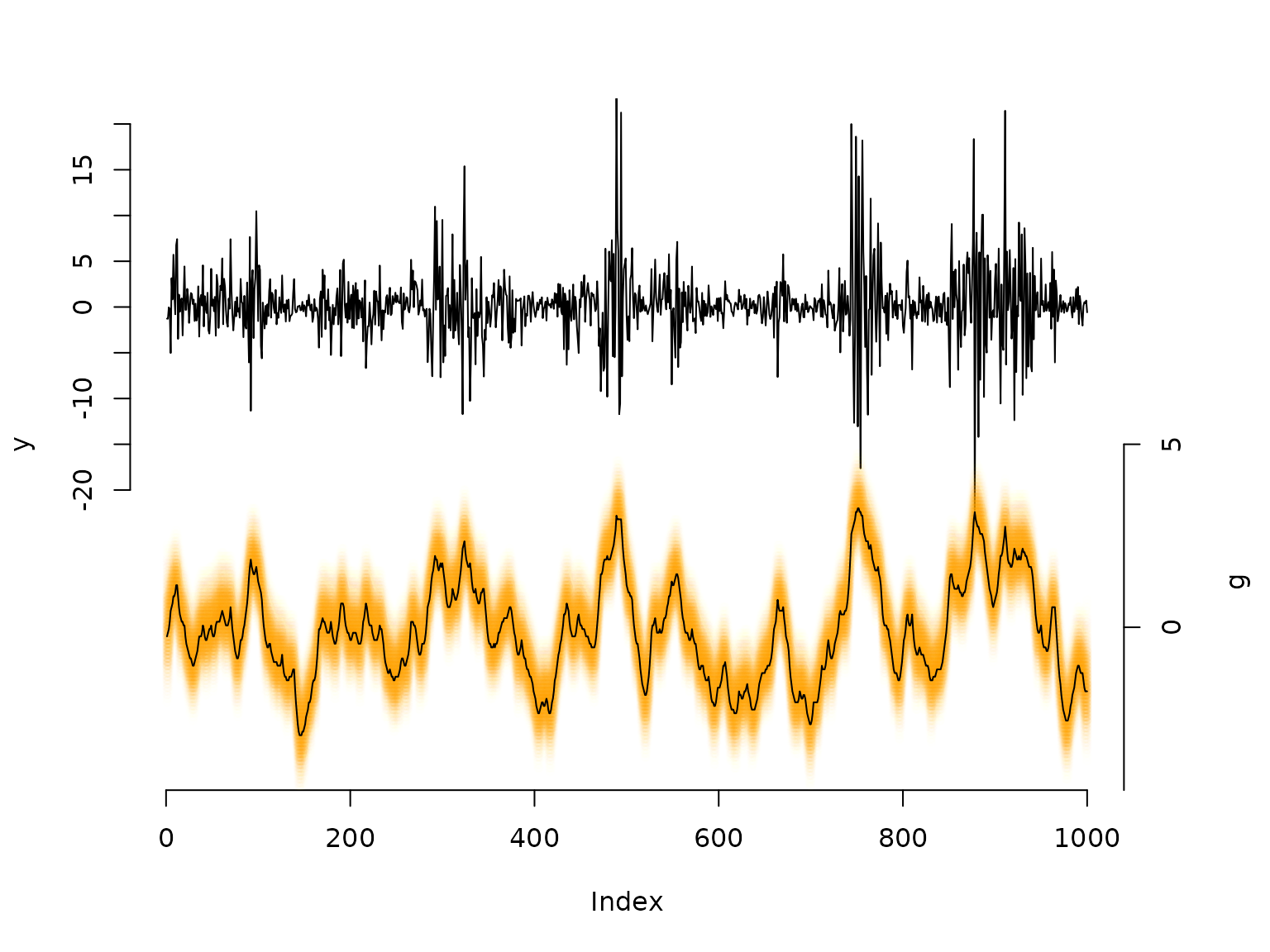

## decoding states

b = seq(-bm, bm, length = m + 1)

h = b[2] - b[1]

bstar = (b[-1] + b[-(m+1)]) / 2

Gamma = sapply(bstar, dnorm, mean = mod$phi * bstar, sd = mod$sigma) * h

delta = h * dnorm(bstar, 0, mod$sigma / sqrt(1 - mod$phi^2))

allprobs = t(sapply(y, dnorm, mean = 0, sd = mod$beta * exp(bstar / 2)))

probs = stateprobs(delta, Gamma, allprobs) # local/soft decoding

states = viterbi(delta, Gamma, allprobs) # global/hard decoding

oldpar = par(mar = c(5,4,3,4.5)+0.1)

plot(y, type = "l", bty = "n", ylim = c(-50,20), yaxt = "n")

# with many states, plotting the full conditional distribution is more informative

# than just the single most-probable state

maxprobs = apply(probs, 1, max)

for(t in 1:nrow(probs)){

colend = round((probs[t,] / (maxprobs[t] * 5)) * 100)

colend[which(colend < 10)] = paste0("0", colend[which(colend < 10)])

points(rep(t, m), bstar * 4 - 35, col = paste0("#FFA200", colend), pch = 20)

}

# Viterbi-decoded path as a summary line

lines(bstar[states] * 4 - 35)

axis(side = 2, at = seq(-20, 20, by = 5), labels = seq(-20, 20, by = 5))

axis(side = 4, at = seq(-5, 5, by = 5) * 4 - 35, labels = seq(-5, 5, by = 5))

mtext("g", side = 4, line = 3, at = -30)

par(oldpar)Comparison to Laplace approximation

An alternative way to marginalise over the continuous state process

is the Laplace approximation, available in

RTMB via the random argument of

MakeADFun(). Instead of discretising the state space, we

write the joint negative log-likelihood — the negative

log of the joint density of observations and states — and declare the

state sequence g_1, \dots, g_T as

random effects. RTMB then integrates them out automatically

using the Laplace approximation.

For the stochastic volatility model the joint negative log-likelihood is

-\ell(\theta,\, g_{1:T}) = -\log f(g_1) - \sum_{t=2}^T \log f(g_t \mid g_{t-1}) - \sum_{t=1}^T \log f(y_t \mid g_t),

where g_1 \sim N(0,\, \sigma^2/(1-\phi^2)), g_t \mid g_{t-1} \sim N(\phi g_{t-1},\, \sigma^2), and y_t \mid g_t \sim N(0,\, (\beta e^{g_t/2})^2).

jnll = function(par) {

getAll(par, dat)

phi = plogis(logit_phi); REPORT(phi)

sigma = exp(log_sigma); REPORT(sigma)

beta = exp(log_beta); REPORT(beta)

jnll = 0

# stationary initial distribution: g_1 ~ N(0, sigma^2 / (1 - phi^2))

jnll = jnll - dnorm(g[1], 0, sigma / sqrt(1 - phi^2), log = TRUE)

# AR(1) state transitions: g_t | g_{t-1} ~ N(phi * g_{t-1}, sigma^2)

jnll = jnll - sum(dnorm(g[-1], phi * g[-length(g)], sigma, log = TRUE))

# observations: y_t | g_t ~ N(0, (beta * exp(g_t / 2))^2)

jnll = jnll - sum(dnorm(y, 0, beta * exp(g / 2), log = TRUE))

jnll

}The state sequence g is included in the parameter list

and declared as random — MakeADFun()

marginalises over it internally.

dat = list(y = y)

par_lap = list(

logit_phi = qlogis(0.95),

log_sigma = log(0.3),

log_beta = log(1),

g = rep(0, n) # random effects initialised at zero

)

obj_lap = MakeADFun(jnll, par_lap, random = "g", silent = TRUE)

system.time(

opt_lap <- nlminb(obj_lap$par, obj_lap$fn, obj_lap$gr)

)

#> user system elapsed

#> 0.196 0.002 0.198

mod_lap = report(obj_lap)

mod_lap$phi # true: 0.95

#> [1] 0.9525517

mod_lap$sigma # true: 0.5

#> [1] 0.4348222

mod_lap$beta # true: 2

#> [1] 2.182106The Laplace approach is typically faster because it avoids the expensive m \times m matrix operations of the discretisation: for a Markov state process the Hessian of the random-effect log-posterior is tridiagonal, so each Laplace step costs O(T) rather than O(m^2 T).

Comparing the two sets of estimates, \hat{\phi} and \hat{\sigma} differ slightly between the two approaches — only at the third decimal place here, and with a single dataset we cannot distinguish approximation error from ordinary sampling variation. In general, however, the Laplace approximation is not exact: it is only exact when the random-effect posterior is truly Gaussian given the fixed parameters, which is never strictly the case because \phi and \sigma enter the likelihood in a nonlinear way. Systematic discrepancies can grow substantially for non-Gaussian state processes such as Markov-switching autoregressive models, or for strongly non-Gaussian conditional distributions such as Bernoulli observations, where the posterior over g is multimodal or strongly skewed.

The discretisation approach makes no such assumption: increasing

m reduces the quadrature error at the cost of computation

time, giving full control over the approximation quality.